SAVILLS: GLOBAL STUDENT HOUSING INVESTMENT BREAKS RECORDS

- New annual global investment volume record of $16.45 bn in 2016

- US reaches new annual investment record of $9.82 bn – up 65% on 2015

- Volumes climb 245% in France and 380% in Germany

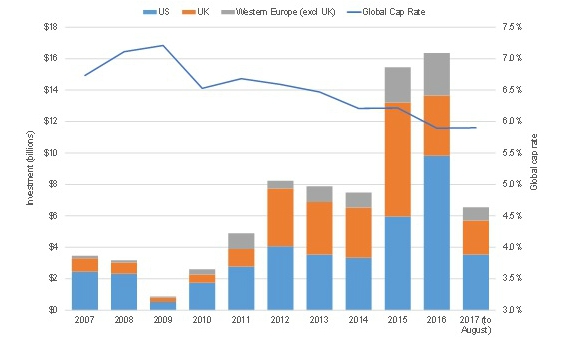

Global investment into institutional student housing broke records in 2016, reaching $16.45 billion and surpassing the previous annual record of $15.6 billion set in 2015, says international real estate advisor Savills.

According to Savills, total volumes by dollar value increased by 5.4% globally in 2016 – double the levels seen in 2014 – as several newly built portfolios of scale traded for the first time and investors continued to recognise the mainstream investment opportunities in the sector and its role as a gateway to other residential assets. Investor interest was focused on the US and UK, the most mature global markets where the majority of investable institutional student housing stock can be found. The US attracted $9.82 billion of investment in 2016, up from $5.96 billion in 2015 - a 65% increase and a new record for the country. The UK secured $3.84 billion investment, its second highest volume ever, after 2015’s record-breaking volume of $7.24 billion.

Proportionally, western European countries saw the greatest growth in investment volumes in 2016, says Savills: student housing investment in France increased by 245% (from €49 million in 2015 to €169 million in 2016) and by 380% in Germany (from €154 million in 2015 to €741 million in 2016). Annual student housing investment volumes in the latter are expected to surpass the €1 billion mark for the first time by the end of 2017, says Savills, with investment volumes across western Europe already up an average of 26% in the first six months of 2017.

Spain, Poland, Hungary, Portugal and the Czech Republic are also attracting attention as increasing volumes of purpose-built student housing are being delivered in these under-supplied markets says Savills, expanding the amount of investable product available in these countries. In September 2017, Spain saw its largest student housing portfolio change hands as AXA Investment Managers-Real Assets agreed to acquire a portfolio of 37 Spanish student accommodation facilities in a JV with US housing investor Greystar and a Dutch institutional investor.

According to Savills, cross-border investors undertook 37% of all global student housing deals in 2016, a higher proportion than the offices (34%) and retail (29%) sectors. In the US, international investors accounted for 39% of total student housing investment in 2016, up from just 1% in 2015.

Global investment into student housing (annual total):

Source: Savills World Research using RCA

Savills says that this is partially due to the student housing investor profile diversifying from largely sovereign wealth funds and private investors to encompass an increasing number of institutions, pension funds and insurance companies, which are investing across multiple jurisdictions in order to achieve scale. Institutional student housing is now viewed firmly as a mainstream asset offering a secure income stream within the residential sector, and as a way to access other residential sub-sectors, such as PRS and senior living, according to Savills.

Student housing yields are currently higher than in many sectors, with the US standing out as particularly high-yielding for such a mature market, says Savills. The international real estate advisor says that yields may harden as institutional involvement increases, the sector matures and perceived risk diminishes. It says there is the potential for a downward yield shift in Australia and Spain in the coming years, and possibly also in Germany, the UK and France, depending on the scope for rental growth in their main university cities.

Student Housing (SH) yields and sector comparison:

|

|

SH prime net initial yield |

10 year govt bonds |

SH yield net of bonds |

Residential (PRS) |

Office Grade A |

|

Australia |

6.00% |

2.6% |

3.4% |

N/A |

6.3% |

|

USA |

5.90% |

2.1% |

3.8% |

5.6% |

5.2% |

|

Spain |

5.75% |

1.5% |

4.2% |

4.4% |

3.5% |

|

Netherlands |

4.75% |

0.5% |

4.3% |

3.4% |

3.4% |

|

France |

4.50% |

0.7% |

3.8% |

3.3% |

3.1% |

|

UK (excl London) |

4.50% |

1.0% |

3.5% |

4.9% |

5.0% |

|

Germany |

4.00% |

0.4% |

3.7% |

3.1% |

3.3% |

|

UK (London) |

3.75% |

1.0% |

2.7% |

3.9% |

4.0% |

Source: Savills World Research

Marcus Roberts, Director of Residential Capital Markets, Europe, at Savills, comments: “Reflecting its popularity with income funds, student housing continues to offer significant potential as an income producing asset class with counter-cyclical qualities. We are currently involved in over €1 billion of mix of development and trading investments across the EU by gross development value, and expect to see more international investment into the US and potentially further consolidation in the UK, with the weak sterling bringing advantages for international buyers. The global capital rate in the sector should remain high as volumes shift toward a higher proportion of high-yielding new and expanding markets. New stock currently being developed in Europe and Australia also paves the way for institutional investment in the future, although investors do need to consider supply and demand at a local level.”

Paul Tostevin, associate director in Savills World Research, adds: “Globally the student housing sector remains in rude health: student numbers continue to rise in France, Germany the Netherlands and Australia; internationalisation strategies for higher education are in place in most major markets; and political uncertainty has done little to alter the sector’s appeal in the UK and US. With provision of student housing still low in many countries, there are numerous opportunities for international providers to bring their expertise to new markets.”